The Risk of Economic Policy Uncertainty on France’s Growth

Economic models predict that uncertainty, following the no-confidence vote and the resignation of the Barnier government, will cause an additional 2% fall in investment. Let’s take a closer look at the methodology used to better understand the figures shaping public debate.

France has been in political turmoil since President Macron announced the dissolution of the National Assembly in June 2024. The subsequent economic consequences have dominated media discussion, with the Barnier government’s resignation on December 5, 2024, adding yet another layer of uncertainty around the country’s political and economic future. Measuring uncertainty and its effects is not straightforward—it needs to be calculated—as no pre-existing figures exist.

First, let’s briefly recall the conceptual difference between risk and uncertainty set out by Frank Knight (1921). Risk refers to a situation where the distribution of probabilities for a series of events is known. In contrast, uncertainty—sometimes called deep or radical uncertainty—describes a situation where there is no way of predicting the likelihood of events. It is a journey into the unknown; the situation about to be experienced has never existed before. Brexit, for example, aligns more closely to the concept of uncertainty, because when it happened, it was the first time that a country had decided to leave the European Union. However, from an empirical point of view, it is very difficult to make the theoretical distinction between risk and uncertainty.

Uncertainty in economic policy

There are various forms of uncertainty, one of which is linked to economic policies. This type of uncertainty has driven many major shocks that have affected the global economy over the recent years, ranging from suspicions of currency manipulation in China to unexpected election results to the Brexit vote. These events generate uncertainty regarding the way economic and social programmes will be implemented—not easily measurable. Recent studies mainly focused on textual analysis and news-based indicators to evaluate uncertainty linked to economic policies.

Nick Bloom and his co-authors were at the forefront of this type of measurement when they developed monthly Economic Policy Uncertainty (EPU) indexes for numerous countries. Their methodology involved looking at the frequency at which certain specific words, or sequences of words, appeared in newspapers in a given country. To be counted, an article had to simultaneously include words relating to the economy (e.g. “economy”, or “economic”), policy (e.g. “deficit”, “central bank”, or “taxes”) and uncertainty (e.g. “uncertain” or “uncertainty”). After standardising and normalising the data, they produced an index, comparable over time and across different countries. This set of EPU indexes constitutes the largest database available for measuring economic policy uncertainty shocks internationally. Figure 1 shows the EPU index for France, from the first quarter (Q1) of 1987 to the third quarter (Q3) of 2024.

We can see that the index has risen continually since the early 2000s, with peaks representing major events such as Brexit in the second quarter of 2016, the height of the Euro debt crisis in summer 2012, and the recent political crisis in France.

The effect on irreversible investment

Macroeconomic effects from uncertainty shocks are numerous, affecting GDP, household consumption, and financial markets. However, the most established framework to measure how fluctuations in uncertainty affect the economy focuses on irreversible investment. The idea is that when investment projects are irreversible—meaning they cannot be “undone” or “modified” without significant costs—investors face a trade-off between the additional returns generated by launching an investment project immediately and the advantages of waiting for more information in the future.

Read also: Are immigrants really taking the jobs of the French (and Americans)?

In the literature, the value of waiting is known as the “real-option value”. Sometimes, it is better to delay new investment projects, and other times it is not. As such, an increase in uncertainty will clearly tip the balance in favour of a wait-and-see approach. By postponing their investments and recruitments, investors will obtain more information about the future, which will increase their chances of making the right decisions, and improve their understanding of the long-term returns on their projects.

A swift recovery after uncertainty?

In his influential 2009 article, Nick Bloom pointed out that increased uncertainty reduces investment, favouring an increasingly widespread wait-and-see approach regarding new investment spendings. However, once uncertainty subsides and economic outlooks become clearer, aggregate activity recovers rapidly, and rebounds a few quarters after the initial shock. This rebound—a short period of above-average growth—is explained by the large-scale return of labour and capital allocations to investment projects, which had previously been suspended.

Numerous recent empirical studies have highlighted the specific role of uncertainty during and after the Great Recession of 2008-2009. For example, in a Bank of France working paper, we evaluated the importance of uncertainty in explaining the weak business investment observed at the end of the global financial crisis, across a sample of OECD countries. Although we concluded that anticipated demand accounted for the majority of the fall in investment (around 80%), we also showed that uncertainty played a significant role, contributing 17% (with the remaining share attributed to the minor role of capital costs).

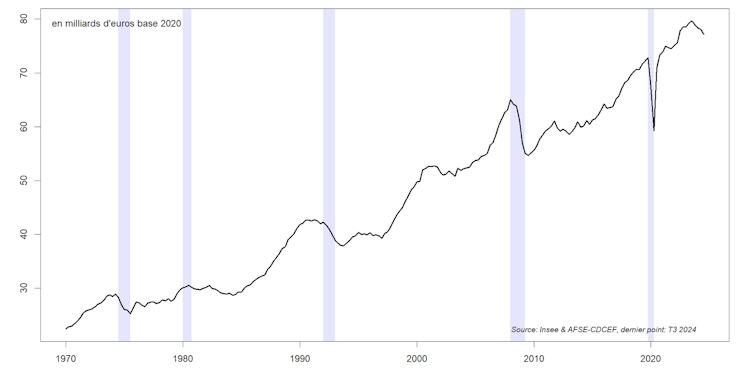

Investment on the decline

In France, corporate investment appears to have been running out of steam over the last year (figure 2). In the third quarter of 2024, the most recent period for which data is available, the annual decline was -3.1%. Investment levels have now fallen for four consecutive quarters. This variable is crucial in evaluating the possibility of a recession in France. It is one of the five variables taken into account by the AFSE’s French Business Cycle Dating Committee, which has established a historical chronology of periods of growth and recession in France since 1970. Therefore, a prolonged and significant decline in this indicator could signal the onset of a possible recession in France.

One might ask to what extent an increase in economic policy uncertainty in France could amplify the fall in investment observed over the past year. To provide a partial response to this question, we can use the Local Projections method to estimate an investment response function to an economic policy uncertainty shock. This requires us to correctly identify the uncertainty shock while controlling for other macroeconomic variables (in this case, GDP and the 10-year government bond yield). When carrying out this exercise, we observe that an increase of one standard deviation (SD) in the EPU indicator leads to a ~0.4% fall in investment, six quarters after the initial shock.

Given that the uncertainty shock observed in the fourth quarter equated to around five SDs, this implies an additional ~2% decline in the level of investment in the next year and a half. Assuming this decline affects all the variables tracked to identify business cycles (GDP, employment, capacity usage rates, and hours worked), this could be a factor signalling an economic recession. Naturally, we hope not to reach that stage, and that a new prime minister, with a clear agenda, will be appointed rapidly, reducing the uncertainty around France’s future economic policy.

This article is republished from The Conversation under a Creative Commons licence. Read the original article in French.